Managing your nonprofit’s finances involves many moving parts. You must create financial policies, distribute responsibilities, develop a budget, and follow relevant guidelines like Generally Accepted Accounting Principles (GAAP).

One of the most important elements of financial management for charitable organizations is nonprofit financial statements. These documents summarize your nonprofit’s financial activities and health, offering benefits like enhanced decision-making, informed strategic planning, better risk management, and increased transparency and accountability.

In this guide, we’ll walk you through the four main financial statements: the nonprofit Statement of Financial Position, nonprofit Statement of Activities, nonprofit Statement of Cash Flows, and nonprofit Statement of Functional Expenses. By understanding the key components of each one, you can compile these documents correctly and provide accurate financial information to donors, board members, staff, grantmakers, and other stakeholders.

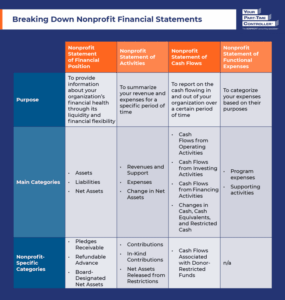

Nonprofit Statement of Financial Position

You may know the nonprofit Statement of Financial Position as a balance sheet. This statement allows you to assess your organization’s financial health through its liquidity and financial flexibility.

Key Components

- Assets. Assets are resources your nonprofit owns or controls. They are often categorized as current and noncurrent. Current assets are items you can convert to cash quickly, such as cash and cash equivalents, accounts receivable, prepaid expenses, and inventory. Noncurrent assets are items you won’t be able to liquidate within the next year, such as land, buildings, and equipment.

- Liabilities. Liabilities are debts or obligations your organization owes. Like assets, liabilities can be current or noncurrent. Current liabilities are short-term debts like accounts payable, accrued expenses, and deferred revenue. Noncurrent liabilities are long-term debts like mortgages or multi-year lease obligations.

- Net Assets. When you subtract your liabilities from your assets, the result is your net assets, which are the financial resources available to your nonprofit. Positive net assets are a sign your organization is financially sound, whereas negative net assets may require you to reevaluate your financial planning. Nonprofits report on net assets with and without donor restrictions to clarify which resources have stipulations on their use and which they can use freely.

Nonprofit-Specific Components

- Pledges Receivable. Similar to accounts receivable, pledges receivable are assets. Pledges receivable represent cash or other assets that people or organizations have promised to contribute to your nonprofit.

- Refundable Advance. A refundable advance is a liability. It refers to cash or other assets with donor-imposed conditions that the nonprofit must return if it fails to meet the stated conditions.

- Board-Designated Net Assets. Board-designated net assets are a form of net assets without donor restrictions. These are funds your board has reserved for specific purposes, such as future programs, investments, contingencies, or asset purchases.

Nonprofit Statement of Activities

The nonprofit Statement of Activities (or income statement) details your revenues and expenses during a specific period. It demonstrates how you manage your resources for your internal staff and external stakeholders to review.

Key Components

- Revenues and Support. Any resources or funds your nonprofit receives fall under this category, including revenue from selling goods or providing services and support from individual contributions and fundraising events.

- Expenses. These are the costs your organization incurs in pursuit of its mission. You’ll break these down into program, management and general, and fundraising expenses.

- Change in Net Assets. The difference between your revenues and expenses is your change in net assets. This number tells you how your financial resources have changed over the reporting period. Similarly to reporting net assets, you’ll record the change in net assets with and without donor restrictions.

Nonprofit-Specific Components

- Contributions. Contributions are financial donations recorded as revenues and support. Nonprofits typically report donor-restricted contributions as restricted revenue or gains, leading to increased net assets with donor restrictions.

- In-Kind Contributions. You’ll separate monetary contributions from in-kind donations, which are nonfinancial donations of goods or services. For example, donors may contribute land, buildings, materials, or supplies. Alternatively, they may offer pro bono professional services like legal or accounting services.

- Net Assets Released from Restrictions. When the stipulations on net assets with donor restrictions are lifted, you’ll reclassify these funds as net assets released from restrictions under the revenues and support category.

Nonprofit Statement of Cash Flows

In the nonprofit Statement of Cash Flows, you’ll report on the cash flowing in and out of your organization over a specific period. You’ll categorize these cash flows depending on whether they come from operating, investing, or financing activities.

Key Components

- Cash Flows from Operating Activities. Operating activity cash inflows include, for example, funds from donations, program fees, grants, and membership dues. Operating activity cash outflows include items like staff salaries and wages, utilities, supplies, and rent.

- Cash Flows from Investing Activities. Cash inflows from investing activities include, for example, any proceeds from investment sales or maturities, whereas cash outflows refer to purchases of investments, property, or equipment.

- Cash Flows from Financing Activities. Typical financing activities include borrowing funds, repaying debts, and issuing or repurchasing equity. Financing activity cash inflows encompass lines of credit and loan proceeds, and cash outflows are debt payments like your mortgage.

- Changes in Cash, Cash Equivalents, and Restricted Cash. Show how your cash flows have changed over the period by reporting your cash, cash equivalents, and restricted cash at the beginning and end of the period.

Nonprofit-Specific Components

Cash Flows Associated with Donor-Restricted Funds. Some of your cash inflows or outflows may stem from donor-restricted funds. Take care to make sure you uphold all donor stipulations and categorize these funds appropriately.

Nonprofit Statement of Functional Expenses

As YPTC’s nonprofit financial statements guide explains, “Nonprofits are required to provide an analysis of their expenses by nature and function. They can choose to do this on the face of their Statement of Activities, as a schedule in the notes attached to the full set of documents, or in a separate financial statement—the Statement of Functional Expenses.”

The nonprofit Statement of Functional Expenses details the nature and function of your expenses, allowing you to be transparent with stakeholders about resource use and easily report expenses on your Form 990.

Key Components

- Program Expenses. Program expenses are costs directly related to the programs and services you provide. For example, books purchased for an educational workshop at a literacy nonprofit would be considered a program expense.

- Supporting Activities. Every other expense falls under supporting activities. These expenses have three main categories:

- Management and General Expenses. These costs relate to your nonprofit’s overall operations and management.

- Fundraising Expenses. These expenses arise from activities related to soliciting contributions and securing grants.

- Membership Development Expenses. These costs are associated with building and maintaining a membership program and may cover things like new member solicitation, membership dues collection, and member relations.

Breaking down the nonprofit financial statements into their respective components allows you to understand, compile, and use these documents. If you need additional assistance developing your financial statements, consider partnering with a nonprofit accounting firm.

About the Author

Jennifer Alleva is the Chief Executive Officer at Your Part-Time Controller, LLC (YPTC), a leading provider of nonprofit accounting services and #65 on Accounting Today’s list of Top 100 accounting firms. Jennifer brings over three decades of expertise in accounting and leadership to her role as CEO of YPTC.

When Jennifer joined YPTC in 2003, the firm consisted of just over 10 staff members. Since then, she has helped grow YPTC into one of the fastest-growing accounting firms in the country.

Jennifer’s accomplishments include her tenure as an adjunct professor at the University of Pennsylvania Fels Institute, her frequent speaking engagements on nonprofit financial management issues, her role as the founder of the Women in Nonprofit Leadership Conference in Philadelphia, and her launch of the Mission Business Podcast in 2021, which spotlights professionals and narratives from the nonprofit sector.

Jennifer Alleva is the Chief Executive Officer at Your Part-Time Controller, LLC (YPTC), a leading provider of nonprofit accounting services and #65 on Accounting Today’s list of Top 100 accounting firms.

Jennifer brings over three decades of expertise in accounting and leadership to her role as CEO of YPTC. A graduate of Boston College and a Certified Public Accountant, Jennifer joined YPTC in 2003 following a career in public accounting with Arthur Andersen and serving as Director of Finance and CFO for several companies. Jennifer was named YPTC Partner in 2007 and served as YPTC Managing Partner from 2018 to 2024.

As an advocate for excellence in nonprofit financial management, Jennifer has dedicated herself to educating Executive Directors and Board members on best practices in the field. Her commitment to advancing the accounting profession and nonprofit sector is reflected in her tenure as an adjunct professor at the University of Pennsylvania Fels Institute, her frequent speaking engagements on nonprofit financial management issues, and her role as the founder of the Women in Nonprofit Leadership Conference in Philadelphia.

When Jennifer joined YPTC in 2003, the firm consisted of just over 10 staff members. Since then, she has helped grow YPTC into one of the fastest growing accounting firms in the country. Throughout this growth, Jennifer has fostered countless opportunities for staff members to grow and expand their skills, contributing to YPTC’s consistent recognition as a Best Place to Work.

Jennifer’s passion for promoting the nonprofit’s mission-driven work extends beyond her professional endeavors. She has served as Treasurer of the Board for Catholic Partnership Schools in Camden, NJ, and has served on the Board of the Greater Philadelphia Cultural Alliance. Jennifer was a charter member of South Jersey Impact100, an organization dedicated to philanthropy and community impact. And, in 2021, Jennifer launched the Mission Business Podcast, which spotlights professionals and narratives from the nonprofit sector.

Jennifer Alleva’s leadership, expertise, and commitment to the nonprofit sector have not only contributed to Your Part-Time Controller, LLC’s significant growth, but have also advanced the field of nonprofit financial management. Through her professional achievements and community involvement, Jennifer continues to empower those dedicated to positively impacting the world.